Short Term Health Plans Biden Rule Limits Duration

Short term health plans Biden rule limit duration: The recent changes to short-term health plans under the Biden administration have sparked a lot of debate. Are these changes good for consumers? Will they impact the insurance market significantly? This post dives into the details, exploring the rule’s impact on both individuals and the insurance industry, and comparing short-term plans to other health insurance options.

We’ll unpack the complexities and try to make sense of it all, so you can understand how these changes might affect you.

The Biden administration’s rationale behind limiting the duration of these plans centers around providing more comprehensive and affordable healthcare options for Americans. However, critics argue that these restrictions limit consumer choice and could lead to higher costs in the long run. We’ll examine both sides of the argument, looking at the potential benefits and drawbacks for various groups of people.

Biden Administration’s Rule Changes on Short-Term Health Plans: Short Term Health Plans Biden Rule Limit Duration

The Biden administration implemented significant changes to the Affordable Care Act (ACA) regarding short-term, limited-duration health insurance (STLDI) plans. These changes aim to increase consumer protections and ensure individuals have access to more comprehensive health coverage. The administration argued that the previous regulations, which allowed for significantly shorter plan durations and limited benefits, left many consumers vulnerable to unexpected medical expenses.

Rationale for Rule Changes

The core rationale behind the Biden administration’s changes centers on protecting consumers from inadequate health coverage. The administration argued that STLDI plans, with their limited durations and exclusions for pre-existing conditions, often failed to provide meaningful health insurance. These plans frequently left consumers with substantial out-of-pocket costs when facing serious illness or injury. Official statements from the Department of Health and Human Services (HHS) emphasized the need to prevent consumers from being misled by the appearance of affordable health insurance that ultimately provided insufficient protection.

The administration cited concerns that the availability of these limited plans undermined the goals of the ACA, which seeks to expand access to affordable, comprehensive health insurance. The changes are intended to clarify the regulations and strengthen consumer protections under the ACA.

Timeline of Rule Changes

While specific dates may vary slightly depending on the specific regulatory element, the process generally unfolded as follows: The administration initially proposed rule changes in [Insert Date of Proposed Rule], following a period of public comment and review, the final rule was published in [Insert Date of Final Rule Publication] and became effective on [Insert Effective Date]. There were [Insert Number] significant revisions made to the rule during the drafting and review process, primarily to address concerns raised by stakeholders.

[Optional: Briefly describe the nature of the revisions].

Key Provisions of the Rule Changes

The following table summarizes the key provisions of the Biden administration’s rule changes concerning short-term health plans:

| Provision | Description | Impact on Consumers | Impact on Insurers |

|---|---|---|---|

| Maximum Duration Limit | Limits the duration of STLDI plans to a maximum of three months. | Reduces the likelihood of consumers facing significant out-of-pocket costs due to gaps in coverage. Increases consumer awareness of the limited nature of the plans. | Restricts the ability to offer longer-term, less comprehensive plans. May lead to adjustments in pricing and product offerings. |

| Pre-existing Condition Exclusions | Prohibits STLDI plans from excluding coverage for pre-existing conditions. | Protects consumers with pre-existing conditions from discrimination and ensures access to necessary care. | Increases the cost of providing coverage for some insurers, requiring them to account for a wider range of health risks. |

| Essential Health Benefits | Requires STLDI plans to cover a broader range of essential health benefits, mirroring those mandated under the ACA. | Ensures consumers have access to a more comprehensive range of essential health services. | Increases the cost of providing coverage for insurers, requiring them to include a wider array of benefits. |

| Renewability Restrictions | Limits the ability to renew STLDI plans beyond the initial three-month period. | Encourages consumers to seek more comprehensive and longer-term coverage. Reduces the potential for consumers to remain on inadequate plans long-term. | Reduces the potential for long-term revenue streams from individual STLDI plans. |

Impact on Consumers

The Biden administration’s rule changes limiting the duration of short-term health plans have significant implications for consumers, altering both the availability and affordability of this type of coverage. Understanding these changes is crucial for anyone considering a short-term plan, as the potential impact on their health and finances could be substantial.The revised regulations primarily affect the maximum duration of short-term plans, reducing the length of coverage allowed.

This directly impacts individuals who previously relied on these plans for extended periods, potentially leaving them with gaps in insurance coverage or forcing them to seek more comprehensive (and often more expensive) alternatives. The changes also affect the types of coverage offered, with limitations placed on the pre-existing condition exclusions and essential health benefits.

Coverage Offered Before and After the Rule Change

Before the rule change, short-term plans offered limited coverage, often excluding pre-existing conditions and many essential health benefits. However, they were significantly cheaper than ACA-compliant plans. After the rule change, the limited coverage remains, but the maximum duration is capped, meaning consumers cannot rely on these plans for as long as they previously could. This means shorter periods of lower-cost coverage, followed by a need to find alternative insurance or face a period without coverage.

The reduction in allowable duration makes these plans less attractive for those needing longer-term, albeit limited, coverage.

Financial Implications for Consumers

The financial impact varies greatly depending on individual circumstances and health needs. While short-term plans were initially attractive due to lower premiums, the limited duration forces consumers to re-enroll more frequently, leading to higher administrative costs and the potential for coverage gaps between plans. Furthermore, the absence of essential health benefits means that consumers might face significantly higher out-of-pocket expenses if they require treatment for conditions not covered by the short-term plan.

The reduced duration also increases the risk of facing high medical bills during periods without coverage.

Hypothetical Scenarios Illustrating Impact

Consider Sarah, a freelance graphic designer, who previously used a short-term plan for 12 months to manage costs. Under the new rules, her coverage is limited to a shorter period, perhaps three months. This forces her to secure new coverage more frequently, increasing administrative burden and the possibility of a gap in coverage. Alternatively, imagine John, a self-employed carpenter, who suffered a workplace injury.

A short-term plan might not cover his rehabilitation costs, resulting in significant out-of-pocket expenses. Finally, consider Maria, a young and healthy individual, who primarily uses a short-term plan for catastrophic coverage. While the reduced duration may not severely impact her immediately, it increases the risk of incurring substantial costs if she experiences an unexpected illness or accident during a period without coverage.

So, Biden’s rule limiting the duration of short-term health plans is a big deal, impacting many people’s access to coverage. This got me thinking about overall health and wellness, and how crucial nutrition is. I was reading this fascinating article about dietary differences between the sexes – check it out: are women and men receptive of different types of food and game changing superfoods for women – and it really highlights how important personalized health approaches are, which makes the limitations of short-term plans even more concerning.

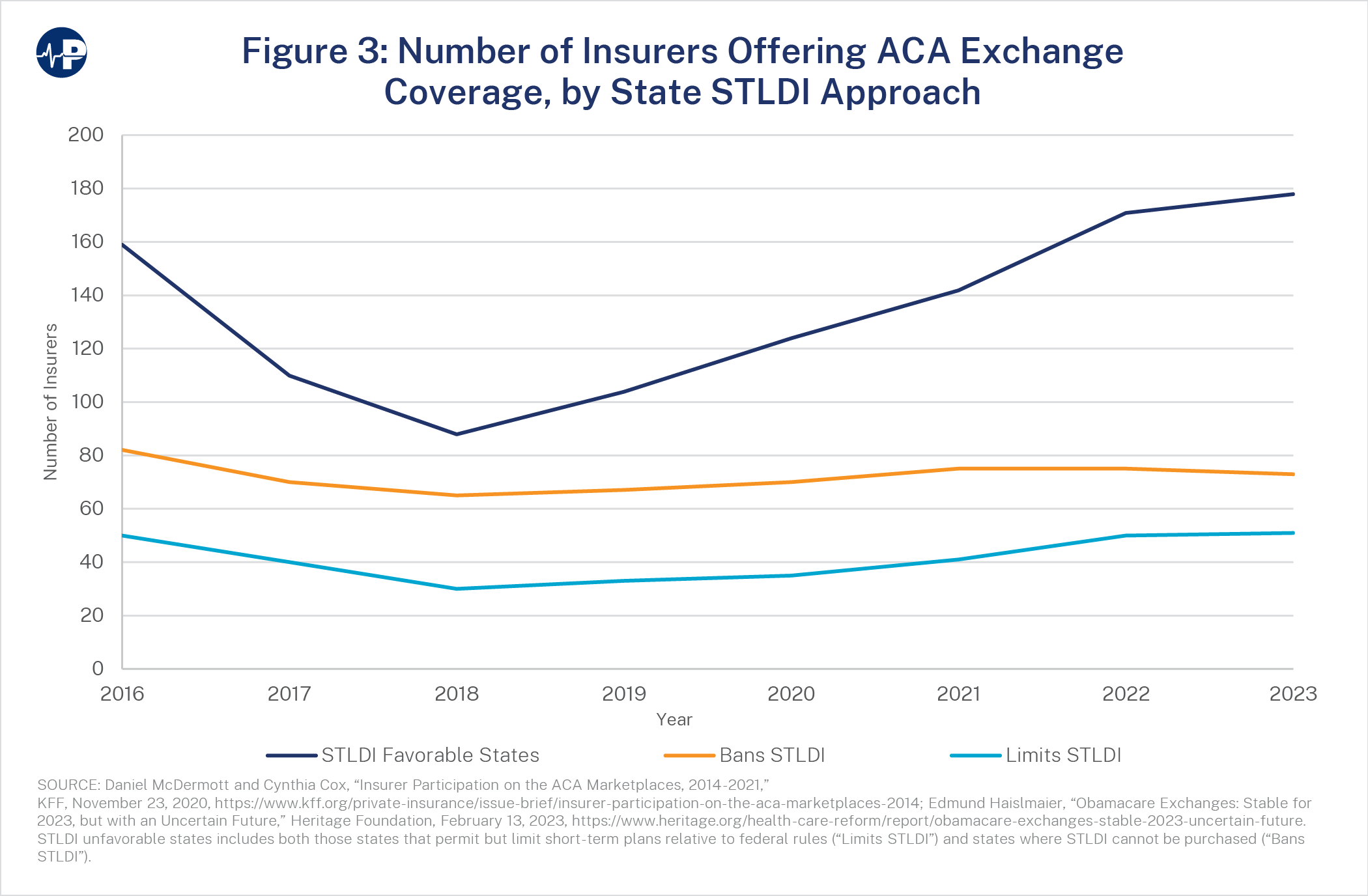

Impact on the Insurance Market

The Biden administration’s rule changes regarding short-term health plans have sent ripples through the insurance market, creating both opportunities and challenges for insurers and consumers alike. The alterations to the allowed duration of these plans directly affect the risk profile for insurers and the availability of options for consumers. Understanding these impacts is crucial for navigating the evolving landscape of health insurance.The most immediate impact is likely to be felt in the number of insurers offering short-term plans.

The Biden administration’s limits on short-term health plans are a concern for many families, especially those facing unexpected medical costs. For example, managing a condition like Tourette Syndrome in children can be expensive, requiring consistent therapy and sometimes specialized care. Finding resources like those offered at strategies to manage Tourette Syndrome in children is crucial, but accessing them becomes harder with restricted health plan options.

Ultimately, the impact of these shorter-term plans on families dealing with chronic conditions like this needs further consideration.

Prior to the rule changes, the longer durations allowed for these plans attracted a larger pool of insurers, as the longer timeframe mitigated some of the risks associated with covering individuals with pre-existing conditions or those likely to require significant healthcare services. With the shorter duration limits now in place, the profitability of offering short-term plans might diminish, leading some insurers to withdraw from the market entirely or significantly reduce their offerings.

This reduction in participation could concentrate the market, potentially leading to less competitive pricing and fewer plan choices for consumers.

Changes in Insurer Participation

The reduced profitability of short-term plans under the new rules could lead to a decrease in the number of insurers offering them. Insurers will carefully evaluate the risk-reward ratio. Companies specializing in short-term plans might be disproportionately affected, potentially leading to mergers, acquisitions, or even bankruptcies. Conversely, larger, more diversified insurers might continue offering these plans, viewing them as a supplementary product within a broader portfolio.

The market share of remaining insurers could also shift, leading to increased concentration. For example, a smaller insurer solely focused on short-term plans might find it financially unsustainable to continue operating under the new rules, while a larger insurer with diverse product lines could absorb the reduced profitability of short-term plans without significant impact.

Effects on Market Competition

The potential reduction in the number of insurers offering short-term plans could significantly impact competition within the market. A more concentrated market might lead to less competitive pricing, reduced plan choices, and potentially less innovation in product offerings. Consumers might face higher premiums and fewer options to choose from, especially in areas with already limited insurer participation. Conversely, some argue that the increased regulation could create a more level playing field for smaller insurers, allowing them to compete more effectively with larger companies.

However, the overall impact on competition is likely to be negative in the short term, at least until the market adjusts to the new regulations.

Impact on Various Stakeholders

| Stakeholder | Potential Positive Impacts | Potential Negative Impacts | Mitigation Strategies |

|---|---|---|---|

| Insurers | Reduced risk associated with longer coverage periods; potential for increased profitability on remaining plans through adjusted pricing. | Decreased market share; reduced profitability; increased administrative burden; potential for withdrawal from the market. | Diversification of product offerings; strategic partnerships; refined risk assessment models; lobbying for regulatory adjustments. |

| Consumers | Potentially lower premiums (if competition remains robust); simpler plan options (fewer choices). | Higher premiums (if competition decreases); fewer plan choices; limited coverage; potential for gaps in healthcare access. | Careful plan selection; comparison shopping; supplemental insurance; advocacy for increased regulatory oversight. |

| Government | Reduced strain on the healthcare system due to shorter coverage periods; potentially fewer uninsured individuals (if individuals opt for more comprehensive plans). | Increased healthcare costs due to uncompensated care; potential for increased demand for public assistance programs; challenges in ensuring equitable access to healthcare. | Increased investment in public health programs; expansion of subsidies for affordable healthcare plans; enhanced consumer education initiatives. |

Comparison with Other Health Insurance Options

Source: paragoninstitute.org

Choosing the right health insurance plan can be a daunting task, especially with the variety of options available. Understanding the key differences between short-term plans, ACA-compliant plans, and government programs like Medicare and Medicaid is crucial for making an informed decision. This comparison will highlight the significant distinctions in coverage, cost, and eligibility to help you navigate this complex landscape.

Short-term plans, ACA-compliant plans, and government programs like Medicare and Medicaid each serve distinct purposes and cater to different needs. While short-term plans offer budget-friendly options with limited coverage, ACA plans provide comprehensive coverage but often at a higher cost. Medicare and Medicaid are government-sponsored programs with specific eligibility criteria, offering varying levels of coverage based on individual circumstances.

Key Differences in Coverage, Cost, and Eligibility

The most significant differences between these plans lie in their coverage, cost, and eligibility requirements. Short-term plans typically offer limited coverage, focusing primarily on hospitalization and accident-related expenses, while excluding pre-existing conditions. ACA plans, on the other hand, are comprehensive and must cover essential health benefits, including preventive care, hospitalization, and prescription drugs. Medicare and Medicaid cover a wide range of services, varying depending on the specific program and individual needs.

Cost varies dramatically, with short-term plans generally being the most affordable but offering limited protection, while ACA plans can be expensive depending on the plan and individual circumstances. Medicare and Medicaid premiums and cost-sharing vary depending on the individual’s income and circumstances.

Comparative Table of Health Insurance Options

The following table summarizes the key features of each plan type to facilitate easier comparison:

| Plan Type | Coverage | Cost | Eligibility |

|---|---|---|---|

| Short-Term Plan | Limited coverage; often excludes pre-existing conditions; may only cover accidents and hospitalizations. | Generally the lowest cost; premiums can vary widely depending on the plan and individual circumstances. | Generally available to anyone; no pre-existing condition exclusions. Duration is limited by law. |

| ACA-Compliant Plan | Comprehensive coverage; includes essential health benefits such as hospitalization, prescription drugs, and preventive care. | Higher cost than short-term plans; cost varies based on plan, location, and individual circumstances. Subsidies may be available based on income. | Available to anyone, regardless of health status. Subsidies based on income. |

| Medicare | Comprehensive coverage for individuals aged 65 and older and certain younger individuals with disabilities. Part A covers hospital insurance, Part B covers medical insurance, Part D covers prescription drugs. | Premiums and cost-sharing vary depending on the plan and individual income. | Individuals aged 65 and older, or younger individuals with certain disabilities. |

| Medicaid | Comprehensive coverage for low-income individuals and families. Coverage varies by state. | Generally low or no cost to beneficiaries. | Low-income individuals and families; eligibility requirements vary by state. |

Impact of Rule Changes on Plan Attractiveness, Short term health plans biden rule limit duration

The Biden administration’s rule changes limiting the duration of short-term plans have significantly altered their relative attractiveness. Previously, the longer duration made them a more appealing option for individuals seeking temporary coverage. Now, with shorter durations, their appeal diminishes, particularly for those needing longer-term coverage. This makes ACA-compliant plans a more attractive option for individuals seeking more comprehensive and longer-term coverage, even if the cost is higher.

For individuals with low incomes, Medicaid remains the most accessible and affordable option, while Medicare remains the primary coverage option for seniors.

For example, a young, healthy individual might have found a short-term plan attractive for a brief period of unemployment. However, with the shorter duration limits, they may now opt for an ACA plan, even with a higher cost, to ensure continuous coverage. Conversely, an older individual nearing Medicare eligibility might find a short-term plan less appealing due to the limitations on coverage and duration.

The rule changes ultimately shift the balance, making ACA-compliant plans and government programs more attractive for a wider range of individuals.

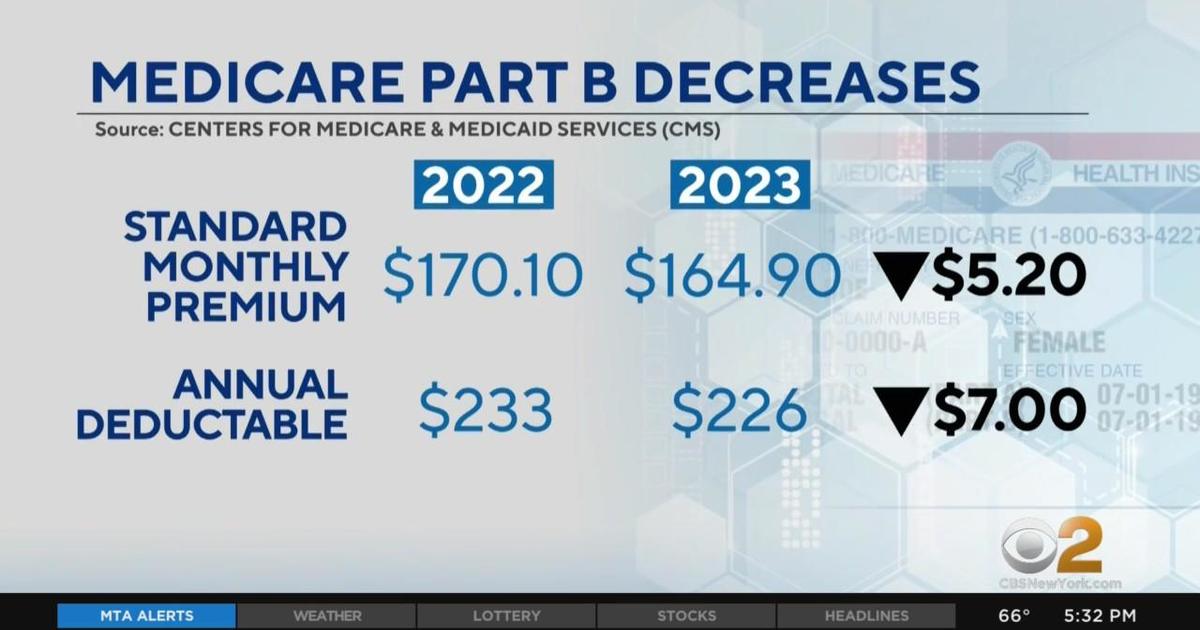

Legal and Political Aspects

Source: cbsnewsstatic.com

The Biden administration’s rule changes regarding short-term health plans sparked immediate and intense legal and political debate. The core issue revolves around the Affordable Care Act (ACA) and its intended balance between affordable healthcare access and market-based insurance options. The changes altered the permissible duration of these plans, impacting both consumers and the broader insurance market. This section explores the legal challenges, contrasting arguments, and court cases stemming from these alterations.The rule changes faced considerable legal scrutiny, primarily focusing on whether they complied with the ACA’s requirements for minimum essential health benefits.

Opponents argued the changes undermined the ACA’s goal of expanding health insurance coverage by allowing plans with limited benefits to compete with comprehensive ACA-compliant plans. Conversely, supporters contended the changes provided consumers with more affordable options, especially those who only needed short-term coverage for specific needs.

Legal Challenges and Court Cases

Several lawsuits were filed challenging the legality of the rule changes. These lawsuits argued that the expanded duration of short-term plans violated the ACA’s provisions regarding minimum essential health benefits. The plaintiffs, often including state attorneys general and consumer advocacy groups, contended that the less comprehensive plans would leave consumers vulnerable to high medical costs. Conversely, the defense emphasized consumer choice and the availability of more affordable options.

The legal battles unfolded in various federal courts, with differing rulings reflecting the complexities of the legal arguments. The ultimate impact of these legal challenges remains to be seen, with potential appeals to the Supreme Court.

Arguments For and Against the Rule Changes

The debate surrounding the rule changes highlighted fundamental differences in political philosophies regarding healthcare.

The Biden administration’s rule limiting the duration of short-term health plans has created a ripple effect, impacting access to affordable healthcare for many. This is especially concerning given the current healthcare landscape, like the situation highlighted in this article about Steward Health Care’s Ohio hospital closures and a Pennsylvania facility at risk: steward ohio hospitals closures pennsylvania facility at risk.

The shrinking availability of healthcare options, coupled with restrictions on short-term plans, leaves many individuals in a precarious position regarding their health coverage.

- Arguments in favor often emphasized consumer choice and affordability. Supporters argued that the rule changes provided more options for individuals who didn’t need or want comprehensive, and often more expensive, ACA-compliant plans. They stressed the importance of market competition and the potential for lower premiums, especially for healthy individuals seeking short-term coverage.

- Arguments against focused on the potential negative consequences for the broader healthcare system. Opponents highlighted the risk of increased uninsured individuals and the potential for higher costs for those who remain insured under ACA-compliant plans. Concerns were raised about the adequacy of the benefits offered by short-term plans, leaving consumers vulnerable to financial hardship in the event of a serious illness or injury.

Furthermore, they pointed to the potential for increased adverse selection within the broader insurance market.

For example, a hypothetical scenario could involve a young, healthy individual choosing a short-term plan to save money, only to face catastrophic medical expenses due to an unforeseen accident. This scenario highlights the core concern of those opposing the rule change. Conversely, a person needing temporary coverage between jobs might find a short-term plan a cost-effective solution. This example reflects the perspective of those who support the rule changes.

These contrasting scenarios illustrate the complexity of the debate and the lack of a simple, universally applicable solution.

Last Word

Source: ytimg.com

Ultimately, the impact of the Biden administration’s rule changes on short-term health plan duration remains to be seen. While the goal is to improve healthcare access and affordability, the long-term consequences for consumers and the insurance market are still unfolding. Understanding the potential implications is crucial for making informed decisions about your health insurance coverage. This post aimed to provide a clear overview of the situation, but remember to consult with an insurance professional for personalized advice.

FAQ Compilation

What exactly are short-term health plans?

Short-term health plans offer limited coverage for a short period, typically less than a year. They usually have lower premiums but also offer significantly less comprehensive coverage compared to ACA-compliant plans.

Are there any exceptions to the duration limits?

There might be some exceptions depending on specific state regulations or individual circumstances. It’s best to check with your state’s insurance department or a qualified insurance agent for clarification.

How can I find out if my current short-term plan is affected?

Contact your insurance provider directly to inquire about the changes and how they might impact your specific plan. You can also review your policy documents carefully.

What are my alternatives if my short-term plan is no longer available?

Consider exploring ACA-compliant plans, Medicaid, or Medicare depending on your eligibility and needs. A health insurance broker can help you find the best option for your situation.