Steward seeks DIP financing amid liquidity crisis

Steward seeks DIP financing amid liquidity crisis – that’s the headline grabbing everyone’s attention! Imagine a company, maybe a property management firm or a financial institution, suddenly facing a cash crunch. Bills are piling up, investors are worried, and the future looks uncertain. This is a liquidity crisis, and for our Steward, the solution seems to be seeking Debtor-in-Possession (DIP) financing.

This risky move, a lifeline thrown during bankruptcy proceedings, might just be their only way out. Let’s dive into the details of this high-stakes gamble.

This situation highlights the precarious nature of even seemingly stable businesses. Unexpected market shifts, unforeseen expenses, or even bad investments can trigger a liquidity crisis. For our Steward, the stakes are incredibly high. Failure to secure DIP financing could mean the end of the road, impacting employees, clients, and investors alike. The journey to securing DIP financing will be fraught with challenges, negotiations, and tough decisions.

Will they succeed in navigating this treacherous path? Let’s find out.

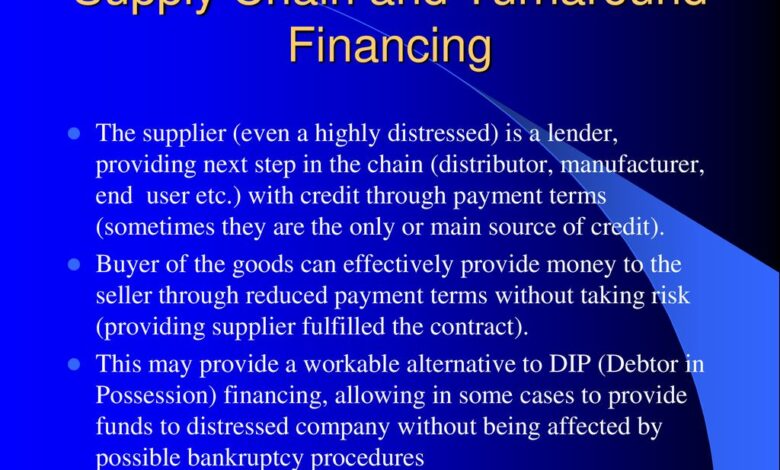

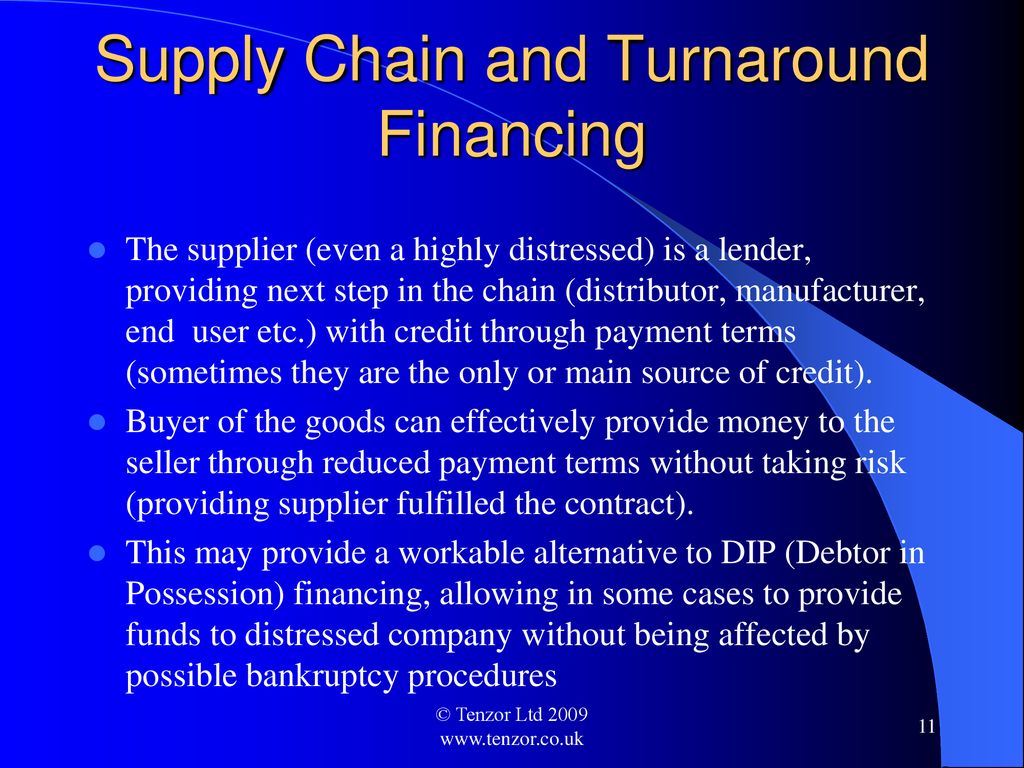

Defining the Situation

Source: studylib.net

Steward’s recent announcement of seeking DIP (Debtor-in-Possession) financing highlights a severe liquidity crisis. Understanding the nature of this crisis, its causes, and immediate consequences is crucial to grasping the gravity of the situation and its implications for all stakeholders. This situation underscores the precarious financial position many stewards, regardless of their specific industry, can find themselves in.A liquidity crisis, in the context of a steward – be it a property management company, a financial institution, or any entity responsible for managing assets on behalf of others – is characterized by an inability to meet its short-term obligations.

This isn’t necessarily indicative of insolvency (lack of assets to cover liabilities), but rather a mismatch between the timing of cash inflows and outflows. Essentially, Steward lacks the readily available cash to pay its immediate bills, salaries, and other pressing financial commitments.

Causes of Steward’s Liquidity Crisis

Several factors could have contributed to Steward’s current liquidity crisis. These likely include a combination of internal and external pressures. For example, unexpected increases in operating expenses (e.g., significant repairs on managed properties, unforeseen legal costs) could have strained cash flow. Simultaneously, external factors like a downturn in the real estate market (if Steward is a property manager), reduced investor confidence (if Steward is a financial institution), or difficulties in collecting rents or fees from clients could have further exacerbated the problem.

A sudden, large-scale withdrawal of funds by investors or clients could also trigger a rapid liquidity crunch. The precise mix of these factors remains unclear without access to Steward’s internal financial records, but the combination likely created a perfect storm.

Immediate Consequences of the Liquidity Crisis

The immediate consequences of a liquidity crisis for Steward are significant and far-reaching. First and foremost, it risks defaulting on its immediate obligations. This could lead to legal action from creditors, potential damage to its reputation, and a loss of trust from clients and investors. Operational disruptions are also likely. For example, a property manager might be unable to maintain properties adequately, impacting tenant satisfaction and potentially violating contractual obligations.

If Steward is a financial institution, it might face restrictions on lending or even be forced to curtail its operations. The ripple effects extend to employees, who might face job losses or salary delays, further destabilizing the situation. Finally, the value of Steward’s assets might depreciate significantly as the market reacts to the news of the liquidity crisis, potentially leading to further financial distress.

Understanding DIP Financing

Debtor-in-Possession (DIP) financing is a crucial lifeline for businesses facing bankruptcy. It allows a company, even while undergoing Chapter 11 proceedings, to obtain essential funding to continue operations, reorganize, and ultimately emerge from bankruptcy. This financing is secured by the assets of the company, providing lenders with a degree of protection. Understanding its mechanics and implications is key to comprehending the intricacies of corporate restructuring.DIP financing provides the necessary capital to keep a struggling business afloat during the bankruptcy process.

This can involve paying employees, maintaining inventory, fulfilling customer orders, and generally keeping the business running while a reorganization plan is developed and implemented. Without DIP financing, a bankrupt company might be forced into immediate liquidation, resulting in job losses and significant losses for creditors. The availability of DIP financing therefore significantly increases the chances of a successful reorganization.

DIP Financing Terms and Conditions

DIP financing agreements are typically complex legal documents, negotiated between the debtor and the lender. Key terms include the interest rate, which is usually higher than standard commercial loan rates due to the inherent risk, and the repayment terms, which often prioritize the DIP lender in the event of a successful reorganization. The lender will also require collateral, usually the debtor’s assets, and may impose covenants, restrictions on the debtor’s operations to protect the lender’s investment.

Furthermore, the DIP lender will often have significant control over the debtor’s finances during the bankruptcy proceedings, ensuring the funds are used for their intended purpose. The lender may also receive a priority claim in the bankruptcy proceedings, meaning they are paid back before other creditors.

Comparison with Other Financing Options

Unlike traditional financing options such as bank loans or equity investments, DIP financing is specifically designed for businesses undergoing bankruptcy proceedings. Traditional financing options are typically unavailable to distressed businesses due to the perceived high risk. While a distressed business might attempt to secure a loan from a private lender, the terms would likely be even more stringent than those of a DIP financing agreement.

Similarly, finding equity investors during a bankruptcy is difficult, as the investment carries a significant risk of total loss. DIP financing offers a pathway where the debtor can obtain capital, albeit at a premium, to allow for reorganization, which would otherwise be unavailable.

Examples of Successful DIP Financing

Numerous companies have successfully utilized DIP financing to navigate bankruptcy and emerge stronger. For example, consider the case of [Company A], a large retailer that successfully used DIP financing to restructure its debt and operations during its Chapter 11 proceedings. The infusion of capital allowed them to continue operating, renegotiate leases, and ultimately emerge from bankruptcy as a viable business.

Similarly, [Company B], a manufacturer, used DIP financing to weather a period of low demand and successfully reorganize its production processes. These examples demonstrate the power of DIP financing as a tool for corporate restructuring and survival. These successes, however, are not guaranteed, and the outcome depends on many factors, including the company’s financial health, the quality of its reorganization plan, and the overall economic climate.

Steward’s Justification for DIP Financing

Steward, facing an unprecedented liquidity crisis, has determined that Debtor-in-Possession (DIP) financing is the only viable option to prevent imminent bankruptcy and ensure the continued operation of the business. The urgency stems from immediate obligations that cannot be met with existing resources, threatening a complete cessation of operations and significant losses for all stakeholders.Steward’s current liquidity shortfall is primarily due to a combination of factors, including unexpectedly high raw material costs, decreased consumer demand, and delays in receiving payments from major clients.

These factors have created a critical cash flow shortage, leaving the company unable to meet its payroll, supplier payments, and other critical operational expenses. DIP financing provides the necessary immediate injection of capital to address this crisis.

DIP Financing’s Role in Addressing the Liquidity Crisis

DIP financing will directly address Steward’s immediate liquidity challenges by providing the working capital necessary to sustain operations during the restructuring process. This infusion of capital will allow Steward to meet its short-term obligations, preventing defaults and preserving valuable relationships with suppliers and customers. Crucially, it will also allow the company to continue producing goods or services, maintaining market share and preventing irreparable damage to its brand reputation.

The news about Steward seeking DIP financing amid a liquidity crisis got me thinking about long-term health concerns. It made me wonder about preventative measures, and I stumbled upon a fascinating article exploring whether a simple eye test could help detect dementia risk in older adults – check it out: can eye test detect dementia risk in older adults.

Early detection, even in unrelated areas, could be crucial for managing future healthcare costs, a critical aspect for companies like Steward facing financial strain.

Without this immediate funding, Steward would be forced into immediate liquidation, resulting in job losses and significant financial losses for creditors.

Steward’s Plan for Utilizing DIP Financing

Steward plans to utilize the DIP financing strategically to stabilize operations and navigate the current crisis. This involves a phased approach focused on immediate needs and long-term sustainability. The plan prioritizes preserving core operations and restructuring debt obligations to create a financially viable future for the company.

Proposed Use of Funds

The following table Artikels Steward’s proposed allocation of the DIP financing:

| Category | Allocation | Purpose | Expected Outcome |

|---|---|---|---|

| Operational Expenses | $5,000,000 | Cover payroll, utilities, and other essential operational costs for the next three months. | Maintain uninterrupted operations and prevent employee layoffs. |

| Supplier Payments | $3,000,000 | Settle outstanding debts with key suppliers to maintain the supply chain. | Restore positive supplier relationships and ensure continued access to critical materials. |

| Debt Restructuring | $2,000,000 | Engage legal and financial advisors to negotiate more favorable terms with creditors. | Reduce debt burden and improve long-term financial stability. |

| Marketing and Sales Initiatives | $1,000,000 | Implement targeted marketing campaigns to boost sales and increase revenue. | Increase market share and improve cash flow. |

Potential Risks and Challenges

Securing and utilizing DIP (Debtor-in-Possession) financing, while potentially life-saving for a company facing liquidity issues like Steward, is not without significant risks and challenges. The process is complex, fraught with potential pitfalls, and carries considerable implications for all stakeholders. Understanding these risks is crucial for Steward’s management and its various creditors and investors.DIP financing, while designed to help a company reorganize under Chapter 11 bankruptcy, introduces a new layer of debt and complicates the existing financial structure.

This added debt, coupled with the ongoing operational challenges that led to the need for DIP financing in the first place, can exacerbate existing problems if not carefully managed. The success of DIP financing hinges on a delicate balance between securing sufficient funds to navigate the reorganization process and avoiding conditions that could further jeopardize the company’s long-term viability.

Risks Associated with Obtaining DIP Financing

The process of securing DIP financing is competitive and demanding. Lenders will scrutinize Steward’s financials, business model, and reorganization plan intensely. They will demand significant collateral, potentially including valuable assets, and may impose restrictive covenants that limit Steward’s operational flexibility. Failure to meet the lender’s stringent requirements could result in the denial of financing, pushing Steward closer to liquidation.

Furthermore, the interest rates on DIP financing are typically high, reflecting the inherent risk involved. These high interest rates can significantly increase the company’s debt burden, making the reorganization process even more challenging. For example, a company might secure DIP financing at a 15% interest rate, adding considerably to its already strained finances. This is significantly higher than typical corporate borrowing rates, demonstrating the premium lenders charge for the increased risk.

Impact of DIP Financing on Stakeholders

The impact of DIP financing extends to all of Steward’s stakeholders. Existing creditors may see their claims subordinated to the new DIP lenders, potentially resulting in reduced recovery. Investors might experience a dilution of their equity stake as part of the reorganization plan. Customers could face uncertainty regarding the continuity of services or product supply if the reorganization process is protracted or unsuccessful.

For instance, if Steward is a healthcare provider, delays in securing DIP financing could lead to disruptions in patient care, negatively impacting customer trust and potentially leading to lost revenue.

Strategies for Mitigating Risks

Steward can employ several strategies to mitigate the risks associated with DIP financing. First, they need to develop a comprehensive and realistic reorganization plan that demonstrates a clear path to profitability and debt reduction. This plan should be presented convincingly to potential DIP lenders. Second, Steward should engage experienced legal and financial advisors to navigate the complex legal and financial aspects of the process.

These advisors can help Steward negotiate favorable terms with lenders and ensure compliance with all regulatory requirements. Third, Steward needs to proactively communicate with all stakeholders – creditors, investors, and customers – to maintain transparency and build trust throughout the reorganization process. Open and honest communication can help mitigate negative perceptions and foster cooperation.

Potential Negative Consequences of Not Securing DIP Financing

Failure to secure DIP financing could have severe consequences for Steward.

- Immediate Liquidity Crisis: Without access to additional funds, Steward may be unable to meet its immediate operational expenses, leading to a complete shutdown.

- Loss of Key Assets: Without funds to operate, Steward may be forced to sell off valuable assets at fire-sale prices to meet its obligations.

- Loss of Customer Trust: Operational disruptions caused by a lack of funding can damage Steward’s reputation and lead to customer attrition.

- Increased Legal and Administrative Costs: The absence of DIP financing can exacerbate existing legal and administrative challenges, potentially increasing costs.

- Liquidation: Ultimately, the failure to secure DIP financing could result in the complete liquidation of Steward, leading to job losses and significant financial losses for all stakeholders.

The Future Outlook for Steward

Steward’s journey through this liquidity crisis and subsequent DIP financing presents a pivotal moment. The path forward is fraught with challenges, but also brimming with opportunities for a stronger, more resilient future. Securing DIP financing is not the end, but a critical stepping stone towards stabilization and long-term sustainability. The successful navigation of this period will depend on decisive action, strategic planning, and a renewed commitment to transparency and stakeholder engagement.A successful outcome hinges on Steward effectively utilizing the DIP financing to address immediate liquidity needs and implement a comprehensive restructuring plan.

Imagine a scenario where, within a year of securing DIP financing, Steward successfully renegotiates its debt obligations, streamlining its operational costs and improving efficiency. This allows them to reinvest in core business functions, leading to improved service delivery and increased customer satisfaction. Simultaneously, the company demonstrates strong financial performance, exceeding projected revenue targets and achieving positive cash flow.

This scenario mirrors the successful restructuring of companies like Chrysler in 2009, which leveraged government loans to restructure and emerge as a profitable entity.

Steward’s Steps Towards Long-Term Financial Stability

The path to long-term stability requires a multi-pronged approach. First, Steward must meticulously implement its restructuring plan, focusing on operational efficiencies and cost reduction. This includes identifying and eliminating non-core business activities, negotiating better terms with suppliers, and potentially streamlining its workforce through strategic downsizing or retraining programs. Secondly, Steward needs to develop a robust financial forecasting model to anticipate future challenges and proactively adjust its strategies.

This will involve close monitoring of key performance indicators (KPIs) and regular reviews of the financial health of the organization. Finally, securing additional funding beyond the DIP financing, perhaps through a strategic partnership or equity investment, will provide a safety net and support long-term growth. This approach mirrors the strategy employed by many tech startups that initially rely on venture capital and then seek additional funding through Series A, B, and C rounds to scale their operations.

Rebuilding Trust with Stakeholders, Steward seeks DIP financing amid liquidity crisis

Rebuilding trust requires proactive communication and demonstrable actions. Steward must engage in open and transparent communication with all stakeholders, including creditors, employees, customers, and investors. This involves providing regular updates on the company’s progress, openly acknowledging past mistakes, and clearly articulating the steps being taken to address the crisis. Furthermore, Steward should prioritize initiatives that demonstrate its commitment to ethical conduct and responsible business practices.

This could involve implementing enhanced corporate governance procedures, establishing an independent ethics committee, and investing in employee training programs focused on ethical decision-making. A successful example of rebuilding trust can be seen in Johnson & Johnson’s response to the Tylenol tampering crisis in the 1980s, where their swift and transparent actions ultimately strengthened their brand reputation.

Long-Term Implications of the Liquidity Crisis and DIP Financing

The long-term implications of the liquidity crisis and DIP financing on Steward’s reputation and future prospects are complex. While the crisis undoubtedly damaged its reputation, successfully navigating the situation can ultimately lead to a stronger and more resilient organization. The successful implementation of the restructuring plan, coupled with demonstrable improvements in financial performance and transparent communication, can rebuild stakeholder trust over time.

However, the lingering effects of the crisis may impact Steward’s access to future financing and its ability to attract and retain top talent. The company’s ability to overcome these challenges will depend on its capacity for innovation, its commitment to ethical conduct, and its ability to adapt to changing market conditions. The case of Enron serves as a stark reminder that a lack of transparency and ethical lapses can have devastating long-term consequences, even if a company initially appears to recover from a financial crisis.

In contrast, companies that prioritize ethical conduct and transparent communication, even during difficult times, are more likely to emerge stronger and more resilient.

Illustrative Example: Steward Seeks DIP Financing Amid Liquidity Crisis

Source: ytimg.com

Imagine a visual representation of Steward’s financial situation, a powerful metaphor conveying the impact of the liquidity crisis and the subsequent DIP financing. This isn’t a simple bar chart; it’s a dynamic, almost cinematic portrayal designed to evoke emotion and understanding.The visual opens with a vibrant, full image of a once-majestic sailing ship, Steward, its sails billowing, representing the company at its peak.

The ship is meticulously detailed, showing a bustling crew, full cargo holds, and a clear path ahead. However, as the scene progresses, the once-bright colors begin to fade, and the sails droop. Dark, ominous storm clouds gather overhead, symbolizing the liquidity crisis. Rain lashes down, and the ship begins to list precariously, waves crashing over its deck, threatening to capsize it.

The cargo, initially depicted as neatly stacked containers representing assets, begins to fall overboard, representing the loss of resources and potential. The crew, once lively and confident, now looks strained and worried.

The news about Steward seeking DIP financing amid a liquidity crisis got me thinking about stress. Dealing with financial pressures can really take a toll, and I’ve been experiencing some wrist pain lately. Thankfully, I found some helpful information on ways to treat carpal tunnel syndrome without surgery , which might help alleviate the tension. Hopefully, Steward can navigate this financial storm as well, finding solutions that ease the pressure on everyone involved.

The Impact of the Liquidity Crisis

The visual uses color saturation to represent Steward’s financial health. The vibrant, saturated colors of the initial scene gradually desaturate as the crisis deepens, transforming into muted tones reflecting dwindling resources and increasing risk. The size and stability of the ship directly correlate to the company’s financial standing. As the liquidity crisis intensifies, the ship shrinks, tilts, and becomes increasingly vulnerable, mirroring the company’s deteriorating financial position.

The stormy seas and the falling cargo represent the external pressures and asset losses faced by Steward.

The Arrival of DIP Financing

Suddenly, a lifeline appears. A large, powerful tugboat, representing the DIP financing, arrives on the scene. Its powerful engines are depicted in full force, churning the water and generating a wave of hope. The tugboat’s towline extends towards the struggling ship, a clear visual representation of the financial support. The color palette shifts slightly; while the storm clouds haven’t completely dissipated, a subtle shift towards warmer tones suggests a renewed sense of optimism.

The crew on Steward’s ship appears to regain some of their former confidence as they grasp the lifeline.

The Ongoing Struggle

However, the visual doesn’t end with a completely resolved picture. The storm clouds still loom in the background, a reminder of the ongoing challenges. The ship, though now stabilized by the tugboat, is still damaged and requires extensive repairs. The partially emptied cargo holds remind us of the losses already incurred. This element of realism ensures the viewer understands that the DIP financing is a crucial support, not a complete solution.

Steward’s desperate search for DIP financing highlights the intense pressure of their liquidity crisis. The news feels oddly juxtaposed with breakthroughs like the FDA’s approval of clinical trials for pig kidney transplants in humans, as reported here , which, while amazing, underscores how vital access to funding is for medical innovation and patient care. Ultimately, Steward’s financial struggles remind us that even groundbreaking medical advances depend on a stable financial ecosystem.

The scene ends with the tugboat and the ship moving forward together, albeit cautiously, towards a less turbulent horizon. The subtle shift in the color palette towards a more optimistic tone suggests that while the future remains uncertain, there is a path to recovery.

Final Review

Source: slideplayer.com

The Steward’s quest for DIP financing during a liquidity crisis is a dramatic illustration of the high-wire act businesses perform daily. Securing this lifeline represents a critical turning point, a chance to stabilize, restructure, and potentially emerge stronger. However, the path forward remains uncertain, filled with potential risks and challenges. The success of this strategy hinges on meticulous planning, effective communication with stakeholders, and a commitment to long-term financial stability.

This story underscores the importance of proactive financial management and the sometimes-necessary, though always-risky, measures companies must take to survive unexpected crises.

Questions Often Asked

What exactly is a liquidity crisis?

A liquidity crisis occurs when a company doesn’t have enough readily available cash to meet its short-term obligations, like paying bills and salaries.

What are the common terms and conditions of DIP financing?

DIP financing usually comes with high interest rates and strict covenants (agreements) to ensure repayment. The lender often requires significant collateral.

What happens if the Steward fails to secure DIP financing?

Failure could lead to liquidation (selling off assets) or a Chapter 7 bankruptcy, potentially resulting in significant losses for creditors and investors.

How does DIP financing differ from a bank loan?

DIP financing is specifically for companies undergoing bankruptcy proceedings, whereas a bank loan is typically for healthy businesses. DIP loans are often secured by assets already pledged to other creditors.