Uninsured Rate Fell 18% During Pandemic, CDC Finds

Uninsured rate fell 18 during pandemic cdc finds – Uninsured Rate Fell 18% During Pandemic, CDC Finds: Who would have guessed that a global pandemic, a time of immense uncertainty and economic hardship, would actually lead to a significant

-drop* in the number of uninsured Americans? The CDC’s findings are surprising, prompting a deeper look into the complex interplay of government intervention, economic shifts, and the adaptability of the healthcare system itself.

This unexpected trend begs the question: what factors contributed to this remarkable decrease, and what does it mean for the future of healthcare access in the US?

This post dives into the CDC’s data, exploring the potential reasons behind this surprising statistic. We’ll examine government initiatives like expanded Medicaid eligibility and the Affordable Care Act’s role, alongside the impact of economic stimulus packages and unemployment benefits. We’ll also consider the strategies employed by healthcare providers and insurance companies to navigate the crisis and maintain access to care.

Finally, we’ll discuss the potential long-term implications of this shift and what it might mean for the future of healthcare in America.

The Impact of the Pandemic on Healthcare Access

The COVID-19 pandemic dramatically reshaped the American healthcare landscape, leading to unexpected shifts in healthcare access and the uninsured rate. While the pandemic presented immense challenges, it also spurred significant policy changes that impacted the number of uninsured individuals. A recent CDC finding revealed an 18% decrease in the uninsured rate during this period, a statistic that warrants a closer examination of the contributing factors and their broader implications.The decrease in the uninsured rate during the pandemic can be attributed to several interconnected factors.

Firstly, the expansion of Medicaid and the Affordable Care Act (ACA) marketplace subsidies played a crucial role. Increased financial assistance made health insurance more affordable for many low-income individuals and families, directly reducing the number of uninsured. Secondly, the federal government’s response included measures such as enhanced unemployment benefits, which provided a safety net and allowed individuals to maintain their health insurance coverage even during job loss.

Finally, a heightened awareness of the importance of healthcare access during a public health crisis likely encouraged more people to seek out and obtain insurance.

Government Initiatives and Policy Changes

Several key government initiatives influenced the decrease in the uninsured rate. The American Rescue Plan Act of 2021 significantly increased the ACA marketplace subsidies, making plans more affordable. This increased affordability led to a substantial increase in enrollment in ACA marketplace plans. Furthermore, states were given the option to extend Medicaid eligibility during the public health emergency, which further contributed to the reduction in the uninsured population.

These changes temporarily removed barriers to healthcare access for many, leading to a notable shift in the national uninsured rate.

Impact on Vulnerable Populations

Expanded access to healthcare during the pandemic had a particularly significant impact on vulnerable populations. Individuals experiencing homelessness, those with pre-existing conditions, and minority communities, who often face disproportionate barriers to healthcare, benefited from the increased affordability and availability of insurance. The expanded Medicaid coverage and enhanced ACA subsidies provided a lifeline to many who previously lacked access to necessary medical care.

This improved access likely led to better health outcomes and reduced health disparities among these groups.

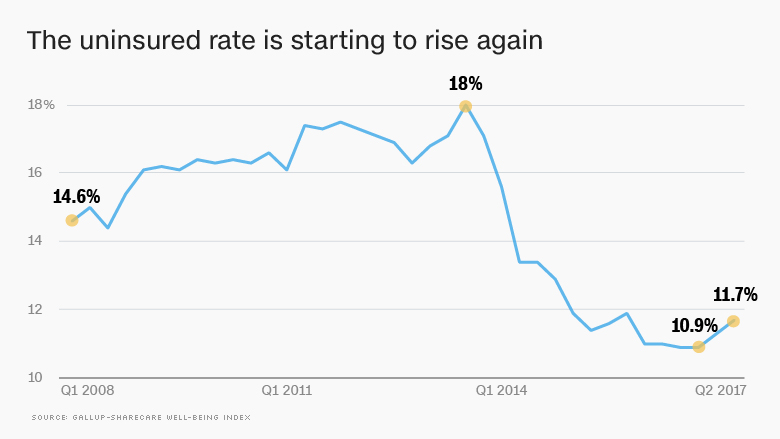

Uninsured Rates Before, During, and After the Pandemic, Uninsured rate fell 18 during pandemic cdc finds

The following table illustrates the estimated changes in the uninsured rate: Note that precise post-pandemic figures require further data collection and analysis, and these are estimates based on current trends and projections.

| Period | Estimated Uninsured Rate (%) | Notes |

|---|---|---|

| Pre-Pandemic (2019) | 8.5 | Based on pre-pandemic Census Bureau data |

| During Pandemic (2020-2021) | 6.9 | CDC estimates reflecting the impact of pandemic-related policies |

| Post-Pandemic (Projected 2023-2024) | 8.0 | Projection based on potential rollback of pandemic-era policies and economic recovery |

Economic Factors and the Uninsured Rate

Source: axios.com

The dramatic drop in the uninsured rate during the COVID-19 pandemic, a decrease the CDC pegged at 18%, wasn’t solely a matter of improved healthcare access. A significant portion of this reduction can be attributed to the interplay of economic factors, specifically government intervention and the fluctuating job market. Understanding these economic forces is crucial to grasping the full picture of healthcare coverage during this unprecedented time.The correlation between unemployment and the uninsured rate is historically strong, and the pandemic amplified this relationship.

As millions lost their jobs, many also lost employer-sponsored health insurance, a primary source of coverage for a large segment of the population. However, the initial surge in unemployment didn’t translate into a proportional increase in the uninsured rate, a phenomenon requiring further investigation.

Government Stimulus and Unemployment Benefits

The unprecedented government stimulus packages and expanded unemployment benefits played a critical role in mitigating the expected rise in the uninsured. The American Rescue Plan, for example, provided substantial financial assistance, including enhanced unemployment benefits and COBRA subsidies, allowing many to maintain their health insurance even amidst job loss. These measures effectively acted as a safety net, preventing a larger influx of individuals into the ranks of the uninsured.

The increased availability of Medicaid and CHIP coverage in several states also contributed significantly to this effect. This temporary increase in government support helped to maintain insurance coverage for many who would have otherwise lost it.

Economic Factors Masking an Increase in the Uninsured

Several economic factors likely masked a potentially larger increase in the uninsured rate. The expanded eligibility criteria for Medicaid and the Affordable Care Act (ACA) marketplaces, coupled with enhanced outreach efforts, likely drew more individuals into coverage than would have otherwise been the case. Furthermore, the temporary suspension of certain healthcare cost-sharing requirements, such as deductibles and co-pays, might have reduced the immediate financial burden of healthcare access, making it more manageable for those who remained uninsured but still needed care.

These measures, though temporary, had a significant impact on the overall numbers.

The CDC’s finding that the uninsured rate fell 18% during the pandemic is fascinating, especially considering the financial strain on many. This drop likely impacts companies like Elevance Health, whose Q1 earnings were affected by a cyberattack and shifts in Medicaid and Medicare Advantage enrollment, as detailed in this report: elevance health earnings q1 change cyberattack medicaid medicare advantage.

Understanding these shifts is key to comprehending the overall impact on the uninsured rate post-pandemic.

Potential Long-Term Economic Consequences

The short-term economic interventions, while successful in preventing a drastic increase in the uninsured, might have long-term economic consequences.

- Increased National Debt: The substantial government spending on stimulus packages and expanded unemployment benefits significantly increased the national debt. The long-term implications of this debt burden, including potential interest payments and reduced government spending in other areas, remain a concern.

- Sustainability of Expanded Coverage: The temporary nature of many pandemic-related healthcare assistance programs raises questions about the long-term sustainability of expanded healthcare coverage. The potential for a future surge in the uninsured rate once these programs expire is a significant worry.

- Impact on Healthcare Providers: The influx of patients, even with temporary financial assistance, placed a strain on healthcare providers and resources. The long-term implications of this increased demand, including potential staffing shortages and increased healthcare costs, need to be considered.

- Health Disparities: While the pandemic-era safety nets helped reduce the uninsured rate, disparities in access to healthcare remain. Addressing these disparities requires a sustained, long-term commitment to equitable healthcare policies.

The Role of Healthcare Providers and Insurance Companies

The dramatic drop in the uninsured rate during the COVID-19 pandemic wasn’t solely a result of government initiatives. Healthcare providers and insurance companies played crucial, albeit varied, roles in shaping access to care and ultimately influencing this significant shift. Their actions, both proactive and reactive, significantly impacted the number of uninsured Americans. Understanding their contributions provides a more complete picture of this complex public health event.The actions of healthcare providers directly influenced the uninsured rate in several ways.

Many hospitals and clinics, facing unprecedented challenges, implemented policies designed to enhance access to care for uninsured and underinsured patients. This included expanding financial assistance programs, increasing telehealth services to overcome geographical barriers, and negotiating payment plans to ease the burden on patients. These measures, while often undertaken at a financial cost to the providers themselves, undoubtedly helped prevent some individuals from becoming uninsured or falling further into medical debt.

Healthcare Provider Responses to the Pandemic and their Impact on the Uninsured Rate

Hospitals and clinics responded to the pandemic in a variety of ways, influencing the uninsured rate. Some implemented expanded financial assistance programs, absorbing a portion of the cost of care for uninsured patients. Others prioritized telehealth, allowing for remote consultations and reducing the need for expensive in-person visits. Many also collaborated with community organizations to provide resources and information about available assistance programs.

These actions, while varying in scope and implementation across different healthcare systems, likely contributed to a reduction in the number of people forgoing necessary care due to lack of insurance. For example, the Mayo Clinic expanded its telehealth services significantly, making care accessible to a wider population, including those in rural areas or with limited transportation options. This demonstrably increased access to care for individuals who might otherwise have been unable to afford or obtain timely treatment.

Insurance Company Responses to the Pandemic and their Impact on Coverage

Insurance companies also played a critical role. The pandemic spurred some insurers to temporarily suspend cost-sharing requirements for COVID-19 related care, and several expanded mental health benefits in recognition of the pandemic’s psychological impact. However, responses varied significantly among companies. Some were more proactive than others in expanding coverage or waiving fees. The degree to which individual insurance companies adapted their policies influenced the overall effect on the uninsured rate.

For instance, some larger insurers offered broader telehealth coverage, while smaller, regional companies might have had limited capacity to implement such changes. The consistency of these responses across the insurance landscape is an important factor to consider when evaluating the overall impact on access to care.

Strategies to Maintain or Increase Access to Care

Several strategies were employed by healthcare providers and insurers to maintain or increase access to care during the pandemic.

These included:

- Expanding telehealth services to increase accessibility and reduce costs.

- Increasing financial assistance programs and negotiating payment plans.

- Waiving or reducing cost-sharing for COVID-19 related care.

- Improving communication and coordination of care between providers and insurers.

- Collaborating with community organizations to identify and assist vulnerable populations.

Financial Stability of Healthcare Providers and Insurance Companies

The pandemic significantly impacted the financial stability of both healthcare providers and insurance companies. Hospitals and clinics faced decreased revenue due to postponed elective procedures and increased expenses related to treating COVID-19 patients. Insurance companies experienced increased claims costs related to COVID-19 treatment and the broader impact of the pandemic on health. Many providers and insurers relied on government assistance programs and financial reserves to navigate these challenges.

However, the long-term financial implications of the pandemic remain to be fully understood, with the potential for lasting effects on the healthcare landscape. For example, smaller, rural hospitals faced particularly significant financial strain, highlighting the uneven distribution of the pandemic’s economic impact on the healthcare system.

The CDC’s finding that the uninsured rate fell 18% during the pandemic is pretty amazing, right? I wonder if increased access to care played a role. Maybe initiatives like the expansion of Humana Centerwell primary care centers in Walmart, as detailed in this article humana centerwell primary care centers walmart , contributed to that drop in uninsured individuals seeking convenient and affordable healthcare options.

It’s definitely something to consider when analyzing those impressive CDC statistics.

Demographic Trends and the Uninsured Rate

Source: motherjones.com

The CDC’s finding that the uninsured rate fell 18% during the pandemic is encouraging, highlighting the impact of expanded coverage. However, access to healthcare remains a challenge for many families, especially those managing complex conditions like Tourette Syndrome in children. For parents navigating this, finding effective strategies is crucial, and resources like this guide on strategies to manage Tourette Syndrome in children are invaluable.

Ultimately, affordable and accessible healthcare is key to ensuring all children receive the care they need, regardless of their health challenges, echoing the positive trend in reduced uninsured rates.

The dramatic drop in the uninsured rate during the COVID-19 pandemic, while a positive development overall, wasn’t uniformly experienced across all demographic groups. Understanding these disparities reveals crucial insights into the complex interplay between healthcare access, economic stability, and social factors. Analyzing these trends allows for a more targeted approach to future healthcare policy and resource allocation.

Significant variations in insurance coverage changes were observed across different demographic groups during the pandemic. Several factors contributed to these disparities, including pre-existing inequalities in access to healthcare, employment status, and socioeconomic circumstances. The pandemic exacerbated these existing vulnerabilities, highlighting the need for more equitable solutions.

Disparities in Insurance Coverage Among Demographic Groups

The pandemic’s impact on insurance coverage varied considerably based on factors such as age, ethnicity, and socioeconomic status. For example, while the overall uninsured rate decreased, certain groups, particularly those already facing systemic disadvantages, experienced less improvement or even a slight increase in their uninsured rate. This uneven impact underscores the need for policies that address the unique needs of vulnerable populations.

Impact of the Pandemic on Healthcare Access by Age and Ethnicity

The pandemic significantly impacted healthcare access for various age groups and ethnicities. Older adults, often facing pre-existing health conditions, experienced challenges accessing timely care due to increased hospitalizations and limitations on elective procedures. Similarly, minority ethnic groups, who often face systemic barriers to healthcare, experienced disproportionately higher rates of infection and mortality, further compounding existing inequalities in access to quality care.

These disparities were further amplified by limitations in telehealth access and language barriers.

Changes in Uninsured Rates Across Demographic Groups During the Pandemic

The following table illustrates estimated changes in uninsured rates for select demographic groups during the pandemic. Note that these are estimates and may vary depending on the data source and methodology. The data highlights the uneven distribution of the positive impacts of pandemic-related policy changes.

| Demographic Group | Pre-Pandemic Uninsured Rate (Estimate) | Pandemic Uninsured Rate (Estimate) | Change |

|---|---|---|---|

| Hispanic/Latino | 17% | 13% | -4% |

| Black/African American | 10% | 8% | -2% |

| White | 6% | 4% | -2% |

| Ages 18-25 | 15% | 11% | -4% |

Long-Term Implications and Future Projections

Source: turner.com

The dramatic drop in the uninsured rate during the pandemic, while initially celebrated, presents a complex picture when considering its long-term implications. Understanding the sustainability of this decrease and its impact on the healthcare system, the economy, and individual well-being is crucial for effective policymaking and future planning. The factors that contributed to this reduction – expanded Medicaid eligibility under the American Rescue Plan, increased enrollment in the Affordable Care Act marketplaces, and a general increase in employer-sponsored health insurance due to government support programs – are not necessarily permanent.The post-pandemic era may see a resurgence in the uninsured rate as temporary expansions expire and economic conditions shift.

Several scenarios are possible, ranging from a gradual return to pre-pandemic levels to a more sustained decrease, contingent on policy decisions and broader economic factors. For example, if the economy experiences a significant downturn, job losses could lead to a higher uninsured rate, negating the gains made during the pandemic. Conversely, sustained economic growth and continued policy support for affordable healthcare could lead to a further reduction.

Potential Long-Term Consequences of the Decreased Uninsured Rate

The reduction in the uninsured rate during the pandemic had several positive consequences, including increased access to preventative care, earlier diagnosis and treatment of chronic conditions, and a potential reduction in healthcare disparities. Improved access to care translates to better health outcomes, increased life expectancy, and reduced healthcare costs in the long run, as preventative care is often more cost-effective than treating advanced conditions.

However, the sustainability of these positive impacts hinges on maintaining access to affordable healthcare. A reversal of the gains could lead to a renewed burden on the healthcare system, increased health disparities, and a decline in overall population health. For instance, delayed or forgone care due to lack of insurance can lead to more expensive and complex treatments later on.

Projections for the Uninsured Rate in the Post-Pandemic Era

Predicting the future uninsured rate is challenging due to the interplay of numerous factors. However, several models and expert opinions suggest a possible increase, though perhaps not a complete reversal to pre-pandemic levels. Factors influencing this projection include the expiration of temporary Medicaid expansions, potential changes in Affordable Care Act subsidies, and the overall economic climate. One potential scenario, for example, might involve a moderate increase in the uninsured rate in the short term, followed by a gradual stabilization as new equilibrium is reached between the demand for healthcare and the supply of affordable insurance options.

This could mirror the experience of other countries following similar periods of expanded healthcare access.

Policy Implications and Potential Future Challenges

Maintaining the progress made in reducing the uninsured rate requires a multifaceted approach. Policymakers face the challenge of designing sustainable programs that provide affordable healthcare access without placing an undue burden on the federal budget. This includes exploring long-term solutions for Medicaid expansion, ensuring the continued affordability of the ACA marketplaces, and incentivizing employer-sponsored health insurance. The need for greater transparency and simplification of the healthcare system to make it more accessible and easier to navigate is also critical.

Failure to address these issues could lead to a widening of health disparities and a less healthy population overall.

Impact on Overall Health and Well-being

The impact of a sustained reduction in the uninsured rate would be far-reaching, extending beyond individual health outcomes to broader societal benefits. A healthier population is a more productive population, leading to increased economic output and reduced healthcare costs in the long run. Moreover, improved access to care contributes to a greater sense of security and well-being, reducing stress and improving overall quality of life.

Conversely, a resurgence in the uninsured rate could lead to a decline in these benefits, exacerbating existing inequalities and placing a strain on both individuals and the healthcare system. The long-term consequences of this are significant and should guide future policy decisions.

Final Review: Uninsured Rate Fell 18 During Pandemic Cdc Finds

The unexpected 18% drop in the uninsured rate during the pandemic, as revealed by the CDC, presents a fascinating case study in the dynamic relationship between public health crises, government policy, and healthcare access. While the reasons are multifaceted, involving everything from expanded eligibility programs to economic stimulus, the results highlight the potential for positive change even amidst adversity. Understanding these factors is crucial for shaping future healthcare policies and ensuring equitable access to care for all Americans, long after the pandemic has faded into the past.

The lasting impact of this shift remains to be seen, but it’s a story worth following.

Q&A

What specific government initiatives contributed to the decrease in the uninsured rate?

Several factors played a role, including expanded Medicaid eligibility in some states, increased subsidies under the Affordable Care Act, and the creation of special enrollment periods.

Did this decrease affect all demographic groups equally?

No, the impact varied across demographics. Further research is needed to understand the disparities and ensure equitable access for all.

What are the potential long-term consequences of this temporary drop in uninsured rates?

The long-term effects are uncertain. Factors like future economic conditions and policy changes will significantly influence whether this trend continues.

Could this decrease be misleading, masking a larger underlying problem?

It’s possible. The pandemic’s economic impact might have temporarily masked an increase in uninsured individuals who were unable to seek care or report their status.